Investor Update

January 5, 2021

Source: FHFA

Additional Resources:

Investor Update

January 6, 2021

Source: Fannie Mae

A summary of Selling Guide, Servicing Guide, and other policy communications

This job aid summarizes recent Selling Guide, Servicing Guide, and related policy updates, clarifications, or other supporting

communications. It provides links to related resources as applicable.

We made many of these changes and communications in direct response to lender feedback

requesting that we simplify or clarify policies or processes.

To download the full matrix, please click source link above.

Disaster Alert

January 1, 2021

Sources:

FOX Carolina (Flooding)

WMAZ CBS 13 (Tornadoes)

Approximate location (according to media outlets) sustaining structural damage:

Tornadoes

– Culloden (Monroe County, 31016)

– Forsyth (Monroe County, 31029)

*Mobile home flipped on Dames Ferry Road

– Musella (Crawford County, 31066)

Flooding

*Impacted ZIP Codes only

– Greenville (Greenville County, 29607)

*Home flooding reported on Lowndes Hill Rd.

MONROE COUNTY, Ga. — Two tornadoes in Monroe County and one in Crawford County touched down in the afternoon of January 1.

According to the National Weather Service, the storm on New Year’s Day triggered several short-lived tornadoes across parts of Central Georgia.

The tornado in Crawford County had winds up to 75 mph and traveled about six miles northwest of Roberta to parts of Musella around 2:20 p.m.

There were multiple trees down along Hopewell Road and Taylor Road. Part of a roof from a home came off in this area as well.

In Monroe County, one tornado had winds up to 85 mph. It traveled about eight miles in Culloden around 2:30 p.m.

Trees were down along Treadwell Road, just before Rogers Church Road. About ten buildings saw damage.

For full report, please click the source link above.

FEMA Alert

December 31, 2020

FEMA issued a Presidential Major Disaster Declaration for areas in Mississippi affected by Hurricane Zeta from October 28-29, 2020. The following counties have been approved for assistance:

Individual Assistance

Public Assistance

Mississippi Hurricane Zeta (DR-4576)

FEMA Declared Disaster Mississippi: ZIP Code List

Additional Resources

FEMA’s web site

FEMA’s Disaster Declaration Process

Safeguard Properties Industry Alerts

VA’s Policy Regarding Natural Disasters

Disaster Alert

December 30, 2020

Source: CNN

Approximate location (according to media outlets) sustaining structural damage:

– Corsicana (Navarro County, 75109, 75110, 75151)

(CNN) – Officials in Navarro County, Texas, said a tornado touched down in the town of Corsicana on Wednesday morning.

The Office of Emergency Management posted on its Instagram page that the area affected is about 100 yards wide and 600 yards long. At least 13 mobile homes were damaged but there were no reports of any injuries at this time, the office said.

They also said that several trees snapped, and two homes were damaged due to trees falling, they said.

The National Weather Service in Dallas confirmed a tornado in Corsicana, likely of EF0 intensity on the Enhanced Fujita Scale, with winds of 65 to 85 mph.

Corsicana is about 50 miles southeast of Dallas.

For full report, please click the source link above.

Disaster Alert

December 28, 2020

Source: Maui Now

Approximate locations (according to media outlets) sustaining structural damage:

Hawaii

– Olowalu (Maui County, 96761)

*Home damage reported on Luawai Street; Church/community center destroyed on Olowalu Village Road (Identified as 801 Olowalu Village Road)

Update 4:35 p.m.: Damage Report from brush fire includes community hall/church

A community hall/church in the Olowalu Village area was completely destroyed, according to a survey conducted Sunday of the impacted area of the brush fire.

Two storage units and two vehicles at the same location also burned and are considered 100 percent losses.

A residence on Luawai Street also sustained fire damage to an exterior wall. Damages to this residence are estimated at $30,000.

Update 11:25 a.m.: Brush fire 90 percent contained.

As of 8 a.m. Sunday, the Olowalu brush fire is considered 90 percent contained. The burn area is estimated at approximately 760 acres.

For full report, please click the source link above.

Safeguard in the News

December 28, 2020

Source: Property Preservation Executive Forum (Winter 2020 Newsletter PDF)

The COVID-19 pandemic was an important topic at this year’s National Property Preservation Conference (NPPC), with property preservation companies and government officials offering updates on managing work while ensuring contractors remain safe. Although the foreclosure and eviction moratoriums were hot topics, the bulk of the discussions focused on preparing for when they are lifted. Speakers and panelists addressed the critical need for businesses to embrace technology to stay relevant and successful in an evolving world, in addition to increased data security as much of the country works remotely.

The discussion also focused on the presidential election and how it will impact servicing, in addition to how to prepare for the predicted influx in volume, foreclosure moratoriums, and post-COVID-19 practices. Participants discussed scaling businesses to align with market conditions. They also addressed the primary drivers of book loss and reducing the loss associated with adverse property conditions, particularly in FHA portfolios.

Other key takeaways from this year’s virtual NPPC focused on improving communications with code enforcement officials to mitigate violations and build relationships. Critical legislative updates also were discussed, including Maine’s Abandoned Properties Act, New Jersey’s proposed maintenance requirement for interior of vacant properties, and New York’s proposed restrictions on property registrations. Best practices for ensuring claims are submitted correctly and timely were explained, specifically for damage reporting, what gets the most disputes on property preservation invoices to servicers, and reporting that has been developed for servicers and property preservation companies to identify gaps in damage assessment process were discussed.

In 2003, Safeguard Properties’ late Founder Robert Klein noticed a lack of industry conferences focused solely on property preservation. While often a topic of conversation, at that time preservation was always a small part of a larger conference. Looking to provide an outlet for industry leaders to collaborate and innovate, Klein began formulating a plan that would bring together all facets of the mortgage field services industry to discuss pressing issues and develop solutions.

In November 2004, the first annual National Property Preservation Conference (NPPC) was held in Washington, D.C. The two-day conference drew leaders from HUD, the GSEs, mortgage servicing, and property preservation companies from across the country. Historic in its spirit of partnership, the conference gained the support needed to ensure its continued success today.

Since the inaugural conference, much has changed. Major disasters, such as hurricanes Katrina, Harvey, Sandy, and countless others, have destroyed communities forcing the nation to come together in restoring those hardest hit. The economy and housing market crashed and continues on a path to recovery, while municipal, state, and federal laws and regulations evolve and change, driving the industry to adapt appropriately.

This year’s pandemic has completely changed the way we preserve properties, so it was imperative to continue these conversations to establish and refine best practices moving forward. As we continue to work our way through the aftermath of these events and changes, one thing is clear: the NPPC continues to be the only outlet for the mortgage field services industry to collaborate on how to best preserve and protect vacant and abandoned properties.

NPPC always draws the top housing industry officials as both speakers and session panelists. The knowledge that is shared can be applied to day-to-day mortgage servicing and property preservation business practices. The discussions fostered each year also allow for serious change and viable solutions.

From information regarding the pandemic to legislative and election discussions, attendees were given tried and true suggestions on adjusting their in-house practices and becoming more efficient with their businesses processes during this year’s NPPC.

Technology will continue to trend in property preservation into 2021 as the focus remains on mobile and automated solutions. It already has given property preservation providers the ability to communicate more efficiently from the field and build our network for scale through aggressive recruiting online. This is imperative to the scalability of processes as we anticipate an increase in REO volume once the moratoriums are lifted.

The expiration of the foreclosure and eviction moratoriums will play a big role in property preservation in 2021. To prepare, property preservation companies continue to provide services through the moratorium as permitted, but also are gearing up in anticipation of spikes so that high quality work continues to be delivered. We have been working on perfecting recruiting techniques. We have also added vendors since COVID-19 at the fastest pace in the history of our company. We continue to shape our scoring, so we have the best vendors spread across our networks and have the best vendors prepped for additional volume.

Investor Update

December 28, 2020

Source: VA

1. Background and Purpose. Under Executive Order 13945, Section 2, of August 8, 2020, it is the policy of the United States to minimize, to the greatest extent possible, residential foreclosures and evictions during the ongoing COVID-19 national emergency. The purpose of this Circular is to extend foreclosure and eviction relief on properties secured by VA-guaranteed loans, including those previously secured by VA- guaranteed loans but currently in VA’s Real Estate Owned (REO) portfolio.

2. Moratorium on Foreclosure and Eviction. Due to the ongoing COVID-19 national emergency and its impact on Veteran borrowers, all properties secured by VA-guaranteed loans, including those previously secured by VA-guaranteed loans but currently in VA’s REO portfolio, are subject to a moratorium on foreclosure and eviction through February 28, 2021. Except with respect to a vacant or abandoned property,

the moratorium applies to the initiation of foreclosures, the completion of foreclosures in process, and evictions.

3. This Circular replaces the following Circulars:

26-20-18: Extended Foreclosure Moratorium for Borrowers Affected by COVID-19;

26-20-22: Extended Foreclosure Moratorium for Borrowers Affected by COVID-19;

26-20-23: Extended Eviction Moratorium for Borrowers Affected by COVID-19;

26-20-29: Extended Eviction Moratorium for Borrowers Affected by COVID-19;

26-20-30: Extended Foreclosure Moratorium for Borrowers Affected by COVID-19.

4. Rescission: This Circular is rescinded October 1, 2021.

Disaster Alert

December 25, 2020

Source: Newsweek

Additional Resources:

News 4 JAX (Damage, power outages in wake of Christmas Eve storms)

Tampa Bay Times (Strong Christmas Eve weather tears through Largo mobile home community)

KSLA News 12 (National Weather Service confirms tornadoes went through Jasper & Newton Counties)

13 News Now (NWS: At least one tornado touched down Christmas Eve in Suffolk)

Approximate locations (according to media outlets) sustaining structural damage:

*Impacted ZIP codes only

Florida

*Wind damage

– Jacksonville (Duval County, 32219, 32223)

*Home damage reported in Dinsmore and Mandarin neighborhoods

– Largo (Pinellas County, 33771)

*Concentrated damage reported in Ranchero Village Mobile Home Park

New Jersey

*Wind damage

– Glen Rock (Bergen County, 07452)

New York

*Flooding

– Maine (Broome County, 13802)

*Homes reportedly “surrounded” by standing water

– Owego (Tioga County, 13827)

– Vestal (Broome County, 13850, 13851)

*Home basement flooding reported

Pennsylvania

*Flooding

– Forks Township (Northampton County, 18040)

– Herndon (Northumberland County, 17830)

– Sunbury (Northumberland County, 17801)

Texas

*Tornadoes

– Kirbyville (Jasper County, 75956)

– Sandjack (Newton County, 75928)

Virginia

*Tornado

– Courtland (Southampton County, 23837)

– Suffolk (Nansemond County, 23437)

*Home damage reported in Holland Community (hardest hit area between Dutch Road, Gates Road and Corinth Chapel Road corridor)

Thousands of people woke up Christmas Day without power after Winter Storm Harold made its way into the northeast, dumping heavy rainfall and strong winds along the East Coast.

The storm has already battered states with massive snowfall and blizzard conditions as it made its way from the mid-Atlantic to the east. The East Coast should expect excessive rainfall throughout the day on Friday before the weather eventually changes to snow by Saturday morning, according to National Weather Service. The organization also warned of chances of flash flooding in the Northeast as the heavy rain mixes with melted snow some states received days ago.

The rain and winds have already left more than 200,000 people without power in New York, Connecticut and Pennsylvania.

For full report, please click the source link above.

Updated 1/5/21: FEMA issued an Emergency Declaration for areas in Tennessee affected by an explosion that took place on December 25, 2020.

FEMA Emergency Declaration Tennessee: ZIP Code List

Updated 1/5/21: The Metro Nashville Codes Department has released the addresses of 10 buildings that have been designated as unsafe.

Restricted access/use:

– 134 2nd Avenue North

– 160 2nd Avenue North

– 166 2nd Avenue North

– 170 2nd Avenue North

– 176 2nd Avenue North

– 178 2nd Avenue North

– 184 2nd Avenue North

Unsafe due to glass (entry not restricted):

– 131 2nd Avenue North

– 144 2nd Avenue North

– 177 1st Avenue North

Source: Nashville Tennessean

Additional Resource:

Damaged Buildings List (Partial)

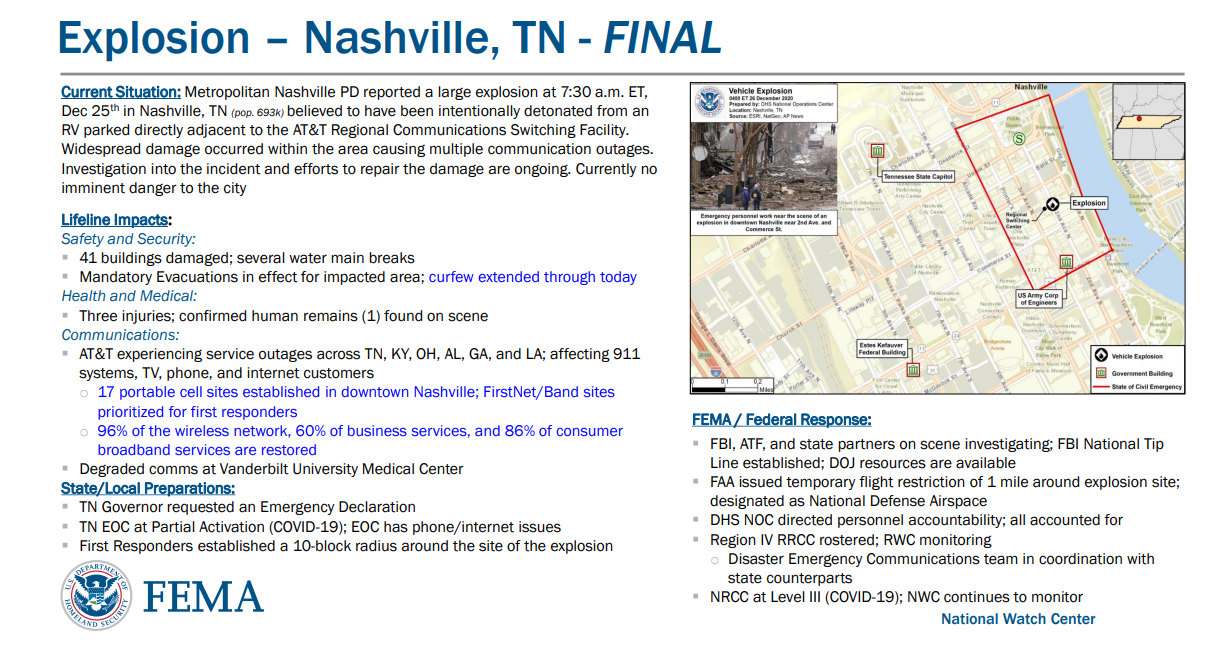

Disaster Alert

December 25, 2020

Source: CNN

Additional Resources:

USA Today (‘Evacuate now. There is a bomb‘)

FEMA (Incident Overview/Response)

Google (Explosion Map)

NOTE: This has not yet been declared a FEMA Major Disaster.

Approximate location sustaining structural damage:

Tennessee

– Nashville: Area of 166 2nd Avenue North (Davidson County, 37201)

(CNN) — The computerized voice coming from the parked white motor home loudly asked people to evacuate and warned that the vehicle would explode in minutes.

Then at 6:30 a.m. local time, it did just that.

The RV’s explosion in downtown Nashville early Friday morning left at least three people injured, set several other vehicles on fire, destroyed a number of buildings on the block and knocked out wireless service in much of the region.

The how and why of the explosion remain a mystery on Saturday, but officials said they are confident the explosion was “intentional.” Still, the Christmas date, the early morning timing and the unusual warnings broadcast on loudspeaker prior to the explosion indicate that this was no attempt at mass murder.

“It was clearly done when nobody was going to be around,” Nashville Mayor John Cooper said Friday.

For full report, please click the source link above.

{kind=link}