Updated 6/17/19: FEMA issued a Presidential Major Disaster Declaration for the Ponca Tribe of Nebraska as a result of severe storms and flooding that took place March 13 to April 1, 2019.

Link to FEMA Alert

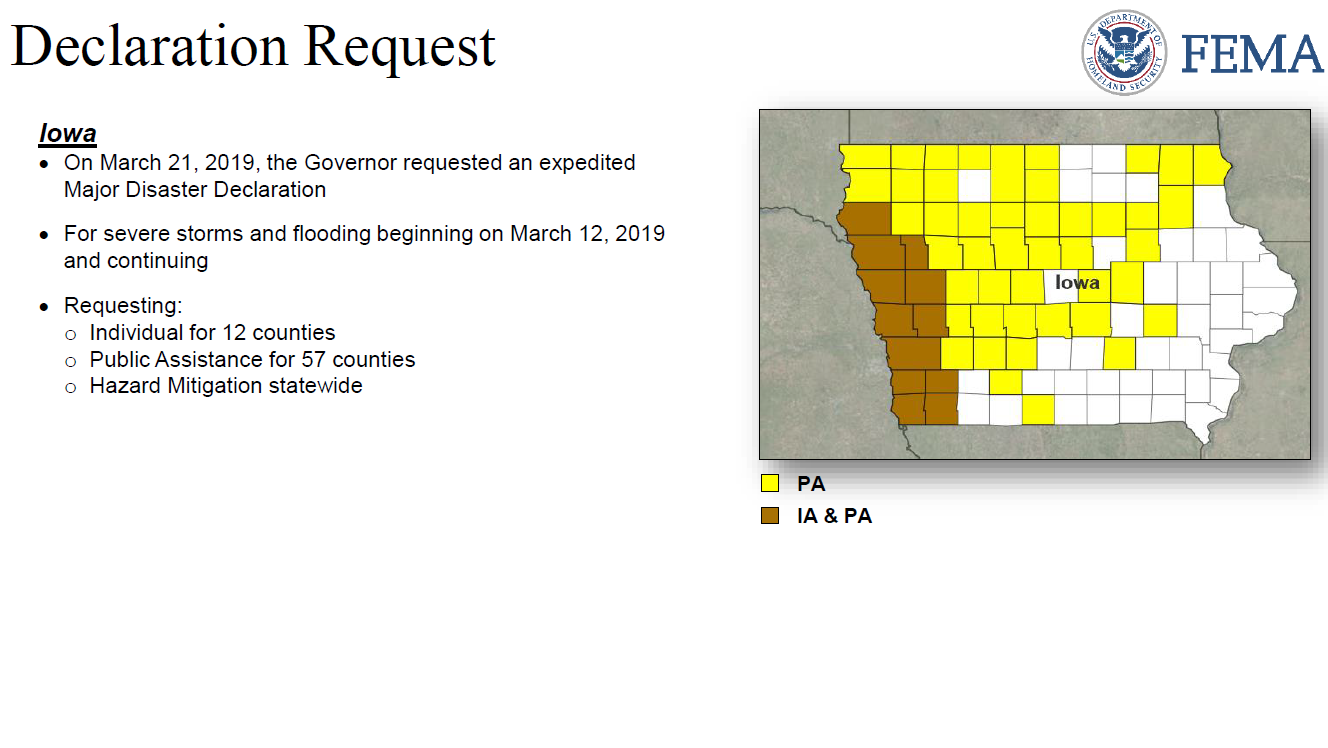

Updated 6/11/19: FEMA issued an update to a Presidential Major Disaster Declaration for areas in Iowa affected by severe storms and flooding that took place March 12 to May 16, 2019.

Link to FEMA Alert

Updated 5/31/19: FEMA issued an update to an Emergency Declaration for areas in Kansas affected by tornadoes and flooding beginning on May 9, 2019 and continuing.

Link to declaration (designated areas)

Associated County ZIP Code List

Updated 5/29/19: FEMA issued an Emergency Declaration for areas in Louisiana affected by flooding beginning on May 10, 2019 and continuing.

Link to Declaration

Associated County ZIP Code List

Updated 5/28/19: FEMA issued an Emergency Declaration for areas in Kansas affected by flooding beginning on May 9, 2019 and continuing.

Link to Declaration

Associated County ZIP Code List

Updated 5/10/19: FEMA issued an update to a Presidential Major Disaster Declaration for areas in Iowa affected by severe storms and flooding beginning on March 12, 2019 and continuing.

Link to FEMA Alert

Updated 5/8/19: FEMA issued an update to a Presidential Major Disaster Declaration for areas in Iowa affected by severe storms and flooding beginning on March 12, 2019 and continuing.

Link to FEMA Alert

Updated 5/7/19: FEMA issued an update to a Presidential Major Disaster Declaration for areas in Iowa affected by severe storms and flooding beginning on March 12, 2019 and continuing.

Link to FEMA Alert

Updated 5/6/19: FEMA issued an update to a Presidential Major Disaster Declaration for areas in Nebraska affected by a severe winter storm, straight-line winds and flooding that took place March 9 to April 1, 2019.

Link to FEMA Alert

Updated 5/6/19: FEMA issued an update to a Presidential Major Disaster Declaration for areas in Alabama affected by severe storms, straight-line winds, tornadoes, flooding and landslides that took place February 19 to March 20, 2019.

Link to FEMA Alert

Updated 4/15/19: FEMA issued an update to a Presidential Major Disaster Declaration for areas in Iowa affected by severe storms and flooding beginning on March 12, 2019 and continuing.

Link to FEMA Alert

Updated 4/15/19: FEMA issued an update to a Presidential Major Disaster Declaration for areas in Nebraska affected by a severe winter storm, straight-line winds and flooding that took place March 9 to April 1, 2019.

Link to FEMA Alert

Updated 4/10/19: FEMA issued an update to a Presidential Major Disaster Declaration for areas in Nebraska affected by a severe winter storm, straight-line winds and flooding that took place March 9 to April 1, 2019.

Link to FEMA Alert

Updated 4/8/19: On April 8, the VA issued a circular that expresses concern about VA home loan borrowers affected by floods in Nebraska, and describes measures mortgagees may employ to provide relief.

Link to Investor Update

Updated 4/5/19: The U.S. Department of Housing and Urban Development (HUD) announced the approval of disaster assistance for the state of Nebraska and will provide support to homeowners and low-income renters forced from their homes in areas affected by severe winter storms, straight-line winds, and flooding.

Link to Investor Update

Updated 4/5/19: The U.S. Department of Housing and Urban Development (HUD) announced that it will speed federal disaster assistance to the state of Iowa and provide support to homeowners and low-income renters forced from their homes in areas affected by severe storms and flooding.

Link to Investor Update

Updated 3/30/19: FEMA issued an update to a Presidential Major Disaster Declaration for areas in Nebraska affected by a severe winter storm, straight-line winds and flooding beginning March 9, 2019 and continuing.

Link to FEMA Alert

Updated 3/29/19: The U.S. Department of Veterans Affairs (VA) issued a circular that expresses concern about VA home loan borrowers affected by severe storms and flooding in Iowa and describes measures mortgagees may employ to provide relief.

Link to Investor Update

Updated 3/27/19: Fannie Mae issued a news release reminding homeowners and servicers impacted by flooding across the Missouri River Basin of available mortgage assistance options.

Link to Investor Update

Updated 3/27/19: Freddie Mac issued a news release reminding mortgage servicers of its disaster relief policies for borrowers affected by flooding in the Midwest.

Link to Investor Update

Updated 3/25/19: The Office of the Comptroller of the Currency (OCC), the Board of Governors of the Federal Reserve System, the Federal Deposit Insurance Corporation, the National Credit Union Administration, and the state regulators issued a joint statement encouraging financial institutions operating in affected Midwest flood areas to meet the financial services needs of their communities.

Link to Investor Update

Updated 3/23/19: FEMA issued a Presidential Major Disaster Declaration for areas in Iowa affected by severe storms and flooding beginning on March 12, 2019 and continuing.

Link to FEMA Alert

Updated 3/21/19: FEMA issued a Presidential Major Disaster Declaration for areas in Nebraska affected by a severe winter storm, straight-line winds and flooding beginning March 9, 2019 and continuing.

Link to FEMA Alert

Updated 3/21/19: Governor Kim Reynolds requested an expedited FEMA Presidential Major Disaster Declaration for areas in Iowa affected by severe storms and flooding beginning on March 12, 2019 and continuing.

FEMA Coverage

Associated County ZIP Code List

Updated 3/21/19: Missouri Governor Michael L. Parson issued a statewide emergency declaration as a result of severe weather and river flooding beginning on March 11, 2019 and continuing.

Link to declaration

Associated County ZIP Code List

Updated 3/20/19: The Weather Channel issued a report outlining initial Midwest flood damage estimates.

Link to report

Updated 3/20/19: Governor Pete Ricketts requested an expedited FEMA Presidential Major Disaster Declaration for areas in Nebraska affected by flooding, rain, high water, wind-driven rain, hail, lightning, straight-line winds and winter storms beginning on March 9, 2019 and continuing.

Media Coverage (KMTV CBS 3)

Associated County ZIP Code List

Please be advised of the following tribal areas included in the above request:

- Omaha Tribe of Nebraska (Public Assistance; Thurston, Cuming, Burt counties)

- Ponca Tribe of Nebraska (Public Assistance; Knox County)

- Sac and Fox Nation (Public Assistance; Richardson County)

- Santee Sioux Nation (Individual/Public Assistance; Knox County)

- Winnebago Tribe (Public Assistance; Thurston, Dixon counties)

NOTE: This has NOT yet been declared a FEMA Disaster.

Updated 3/20/19: The Nebraska Emergency Management Agency (NEMA) announced additional counties covered under an emergency declaration.

NEMA on Twitter (declaration updates)

Updated County ZIP Code List

Flood damage estimates/information (NEMA)

Updated 3/19/19: The Weather Channel issued a report offering an update on extreme river flooding affecting the Midwest.

Link to report

Updated 3/19/19: Iowa Governor Kim Reynolds issued a supplemental emergency proclamation adding five additional counties impacted by flooding and flash flooding.

Link to proclamation

Updated County ZIP Code List

Updated 3/19/19: The Nebraska Emergency Management Agency (NEMA) announced additional counties covered under an emergency declaration.

NEMA on Twitter (declaration updates)

Updated County ZIP Code List

NOTE: This is independent from any FEMA Disaster Declaration.

Disaster Alert

March 17, 2019

Source: NBC News

Additional Resources:

Related Governor Emergency Declarations:

Iowa

Declaration (3/14/19)

Supplemental Declaration (3/15/19)

Associated County ZIP Code List

Kansas

Declaration (KPR 3/17/19)

Associated County ZIP Code List

Nebraska

Declaration (3/15/19)

Associated County ZIP Code List

South Dakota

Declaration (3/15/19)

Associated County ZIP Code List

Wisconsin

Declaration (3/15/19)

Associated County ZIP Code List

NOTE: The above declarations are independent from any FEMA Disaster Declaration.

Flood warnings and advisories remained in effect Sunday evening across eastern Nebraska, southern Wisconsin and parts of Iowa. The NWS said major flooding was expected to continue across the region as late as Wednesday.

The Missouri River reached 30.2 feet in Fremont County in far southwestern Iowa on Sunday, breaking the record by 2 feet and topping levees in the towns of Bartlett and Thurman. A levee was breached on the Platte River near North Bend, northwest of Omaha, Nebraska, on Sunday afternoon; authorities urged all residents to move to higher ground immediately.

Nebraska Emergency Management Agency said Sunday it was monitoring 17 flood locations across the state and expected more record crests in the next 24 to 48 hours.

Also on Sunday, Iowa Gov. Kim Reynolds said 38 counties have received a disaster proclamation and more than 110 homes were damaged by floods in the western city of Hornick. She and the governors of Nebraska and Wisconsin all declared states of emergency.

For full article, please click the source link above.

{kind=link}